If all of your savings live in one place, such as one general savings account, how do you decide what that money is actually for?

Maybe it is meant for emergencies. Maybe you use it when an expense comes up that you forget about, or it gets used for a little bit of everything.

Saving money is always better than not saving. But when everything is kept in one place, it can become harder to tell what your savings are meant to cover or how close you are to specific goals.

This is where understanding the difference between an emergency fund and a sinking fund becomes helpful.

What Is an Emergency Fund?

An emergency fund is money set aside for unexpected expenses that need to be handled right away.

Common examples include:

- Job loss or a sudden drop in income

- Medical emergencies

- Major car or home repairs that cannot wait

An emergency fund acts as a financial cushion so you can handle the unexpected without going into debt.

What an emergency fund is meant to do

An emergency fund is there to give you breathing room when something unexpected happens.

More specifically, an emergency fund helps you:

- Cover urgent expenses without relying on credit cards when there is no clear plan to pay the balance off and avoid interest

- Protect your regular budget from being thrown off

- Avoid turning a short-term problem into long-term debt

It is not meant to be used often.

If you want a deeper breakdown of how to build an emergency fund, including how much to save and where to keep it, I walk through that step by step here.

What an emergency fund is not for

An emergency fund is not meant to cover vacations, holidays or gifts, planned car maintenance, or annual bills and subscriptions.

These types of expenses are better handled through sinking funds, which we will talk about next.

Ideally, your emergency fund sits untouched until you truly need it. The goal is for one surprise not to turn into a long-term setback.

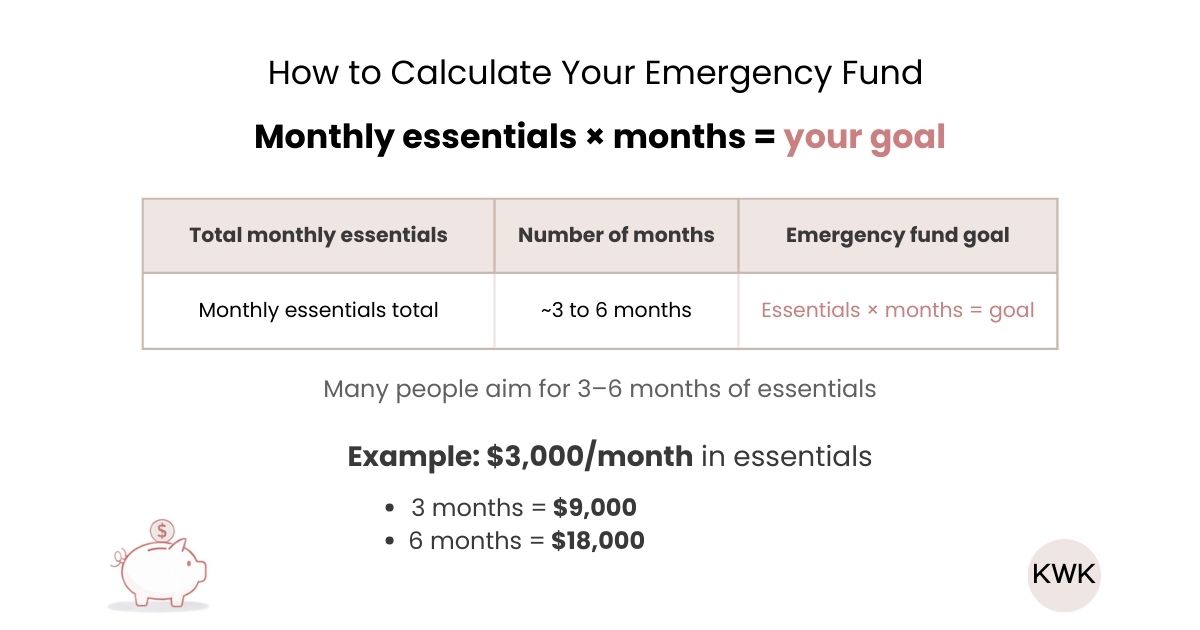

How much should an emergency fund be

You will often hear recommendations like three to six months of essential expenses. This is a helpful guideline, not a strict rule.

The right amount for your emergency fund depends on things like:

- How stable your income is

- Whether you have dependents

- Your job security

- Your overall comfort level with risk

- Other savings you already have in place

At a high level, your emergency fund is based on your essential monthly expenses and how many months of coverage you want.

For example, if your essential expenses are $3,000 per month and you aim for three months, your emergency fund target would be $9,000.

If you are just starting, build your emergency fund gradually. Smaller, consistent contributions add up over time.

What matters most is that your emergency fund gives you peace of mind and helps you feel confident handling surprises when they come up.

What Is a Sinking Fund?

A sinking fund is money you save intentionally for expenses you know are coming.

These are not emergencies. They are planned or predictable expenses that can throw off your budget when you do not prepare for them ahead of time.

Common sinking fund categories include:

- Travel

- Holidays and gifts

- Car maintenance or repairs

- Annual bills

- Home projects or big life milestones, like weddings

The key difference is timing. With sinking funds, you know the expense is coming, even if you do not know the exact date.

What a sinking fund is meant to do

Sinking funds help you spread out the cost of larger expenses over time.

Instead of pulling from your emergency fund or putting the expense on a credit card without a clear plan to pay it off right away, you save for it little by little ahead of time.

That way, sinking funds help you:

- Plan for expenses you already know are coming

- Pay for them without touching your emergency fund

- Avoid surprise spending that throws your budget off

Because these expenses are expected, sinking funds are meant to be used. When the expense comes up, you know that money was set aside for it, so there’s no second guessing.

For a full breakdown with examples and step-by-step guidance, check out my complete guide on how to start sinking funds.

Sinking Fund vs Emergency Fund: The Key Differences

This sinking fund vs emergency fund comparison shows how each type of savings serves a different role.

Here is the simplest way to see the difference:

| Emergency Fund | Sinking Fund |

| Used for unexpected expenses | Used for planned expenses |

| Usually one separate account with a single purpose | Often broken into multiple saving accounts or buckets, each with its own purpose |

| Used rarely | Used regularly |

| Covers true emergencies and protects you during financial surprises | Covers planned expenses and helps prevent surprises from throwing off your budget |

| Not used for everyday or planned spending | Used intentionally for specific goals or expenses |

An emergency fund protects you from the unexpected.

A sinking fund helps you plan ahead for expenses you already know are coming.

Both matter, and together they make your savings clearer and easier to manage.

Do You Need Both Types of Savings?

Yes, most people benefit from having both because each serves a different purpose.

Emergency funds are there for the unexpected.

Sinking funds handle expenses you already know are coming.

When everything lives in one general savings account, that money often ends up doing too much. It gets used for planned expenses, then feels off-limits when a real emergency comes up.

Having both keeps things clear. Each type of savings has a specific job, so you know what your money is for and when to use it.

Which Should You Build First?

If you are starting from scratch, an emergency fund usually comes first.

That does not mean you need to fully fund it before starting sinking funds. Once you have a small amount you feel comfortable with as a buffer, you can begin planning for upcoming expenses at the same time.

An emergency fund gives you stability.

Sinking funds are what help everything work together.

You do not need dozens of accounts or a complicated system. A simple setup might look like this:

- One savings account for your emergency fund

- One savings account with labeled buckets for planned expenses, or separate savings accounts for different sinking fund categories

Your emergency fund is there for true surprises.

Your sinking funds move in and out as life happens.

This keeps your savings organized, so you are not constantly wondering if you have enough saved or what money you can use.

The Bottom Line

You do not have to choose between a sinking fund and an emergency fund. They do different jobs, and having both helps your savings make more sense.

When each part of your savings has a purpose, it is easier to plan, spend, and save without overthinking every decision.

Together, they create a system that supports intentional money planning and gives you more clarity around your money.