Paying off credit card debt can feel confusing. You might be making payments every month, but the balance barely moves or even increases. That usually happens because high interest and minimum payments can keep the balance from going down as quickly as you would expect.

That is what makes credit card debt especially frustrating. You can be doing the right things and still not see results. The good news is that paying off credit card debt is possible, even if you are starting small.

This post breaks down how to pay off credit card debt step by step, including how to choose the right payoff method and avoid common mistakes.

Why Credit Card Debt Is So Hard to Pay Off

Credit card debt is hard to pay off because of how credit cards are designed.

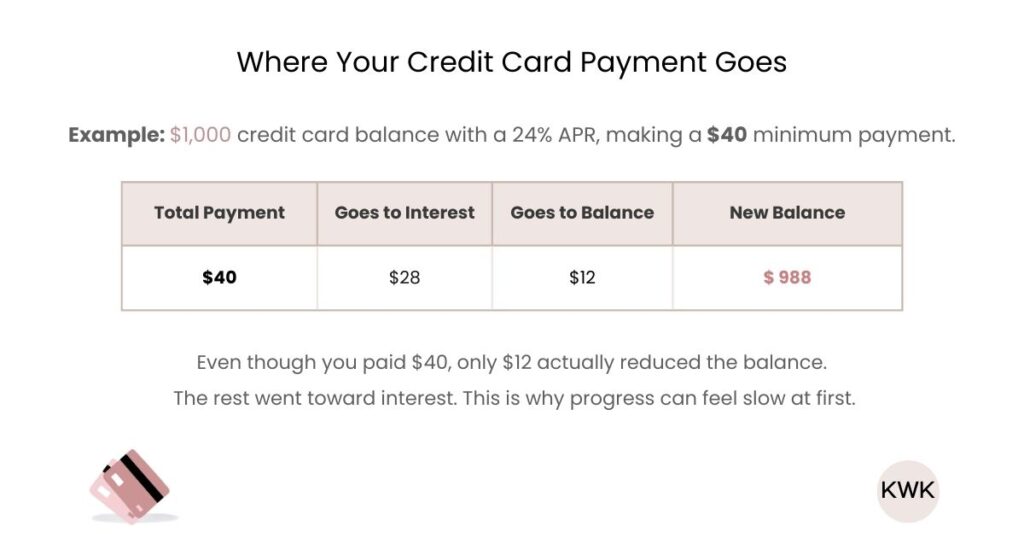

Credit cards have interest rates, usually much higher than other types of debt, often 18% or higher. Interest is charged on whatever balance is left on your card, and with most credit cards, that interest compounds daily. This means a large part of each payment can go toward interest instead of the balance, which is why it can feel like you are not getting anywhere.

Minimum payments also slow progress. They are set low to keep your account in good standing, not to help you pay the debt off quickly. Paying only the minimum can stretch repayment out for years and lead to paying more than you originally borrowed because of interest.

This is why having a clear debt payoff plan for credit cards matters. Understanding how interest and minimum payments work helps you make decisions that move your balance in the right direction.

Step 1: Get Clear on Your Credit Card Balances

Before you think about paying off credit card debt fast, it helps to get clear on the numbers.

Write down:

- Each credit card

- Current balance

- Interest rate (APR)

- Minimum payment

You can use a piece of paper, a planner, or a spreadsheet. If you want something simple, you can use my debt payoff spreadsheet.

This step is not about judging yourself. It is about seeing everything in one place. Once you do that, the numbers usually feel less overwhelming and easier to deal with.

Step 2: Choose a Credit Card Debt Payoff Method

Once you know your balances, the next step is choosing how you want to pay them down.

There are two common credit card debt payoff methods. Both work. The best one is the one that fits how you think and is easiest for you to stick with.

The Snowball Method

With the snowball method, you focus on paying off the card with the smallest balance first, regardless of interest rate.

You pay the minimum on the rest and put any extra money toward that smallest balance.

This method works well if:

- You like quick wins

- Seeing early progress helps you stay motivated

- You want the process to feel more doable

The Avalanche Method

With the avalanche method, you focus on paying off the card with the highest interest rate first.

You still pay the minimum on the rest, but any extra money goes toward the card costing you the most in interest.

This method works well if:

- You want to save more on interest over time

- You are more numbers-driven

- You are okay with progress feeling slower at the beginning

Snowball vs Avalanche for Credit Cards

When deciding between the snowball vs avalanche method for credit cards, it helps to think about what keeps you consistent.

If motivation is your biggest challenge, the snowball method often works better.

If discipline comes more easily to you and you like the math side of things, the avalanche method may make more sense.

Pick one method that works best for you and give it time to work.

Step 3: Build a Realistic Credit Card Debt Payoff Plan

Once you know your balances and have chosen a payoff method, the next step is turning that into a plan you can actually follow.

Start with two priorities:

- Decide how much extra you can put toward your focus card, based on the method you chose

- Keep paying the minimum on all other cards

Your focus card is:

- The card with the smallest balance if you are using the snowball method

- The card with the highest interest rate if you are using the avalanche method

Any amount above the minimum helps. The goal is not to be extreme, but to be consistent.

How Much Extra Should You Pay?

This is where a lot of people start to overthink.

This is where your budget comes in. Look at what is already going out each month and decide what you can realistically redirect toward your focus card.

The goal is not to cut everything you enjoy. It is to pull back on the things that matter less or do not really bring you joy, so the plan feels sustainable.

Look at your budget and decide what feels realistic to commit to each month. Then think about where that money can come from. It might be:

- A subscription you no longer use

- A few meals at home instead of eating out

- A short pause on extra spending

Even an extra $25 or $50 a month can make a real difference when it goes toward one card consistently.

Paying off credit card debt is less about intensity and more about sticking with a plan you can maintain, without burning yourself out.

What to Do When a Card Is Paid Off

When one card is paid off, take the full payment you were making on that card and apply it to the next card on your list. You roll that payment forward.

This is how momentum builds. Your total monthly payment stays the same, but more of it goes toward your next balance without needing to find extra money.

Quick Example

Let’s say your focus card is Card A.

- Card A minimum payment: $35

- Extra you were adding: $65

- Total you were paying on Card A: $100

Once Card A is paid off, you take that full $100 and apply it to Card B (while still paying minimums on everything else).

If Card B has a $40 minimum payment, your new payment becomes $140. ($40 minimum + $100 rollover).

If you want a full, step-by-step breakdown of how this works, I explain each payoff method in more detail in my posts on the snowball method and the avalanche method.

Common Credit Card Debt Payoff Mistakes to Avoid

Paying Cards Randomly Instead of Following a Plan

Putting extra money toward different cards each month can feel productive, but it usually slows progress. Following one clear payoff method helps your payments work together instead of against each other.

Only Paying the Minimum and Expecting Fast Results

Minimum payments are designed to keep your account in good standing, not to pay the balance down quickly. If you are only paying the minimum, progress will be slow, even if you are consistent.

Using Balance Transfers or Loans Without Changing Habits

Balance transfers and personal loans can be a helpful way to lower interest or simplify payments. When used intentionally, they can save you money and help you make faster progress.

The problem comes when the balance moves, but the habits do not.

If spending habits do not change, it is easy to end up with new credit card balances on top of the loan or transfer. That is when things start to feel worse instead of better.

These tools work best when they are part of a clear payoff plan and the cards being paid off are no longer being used. They are meant to support your progress, not reset the clock.

Trying to Be Too Aggressive Too Fast

Cutting everything from your budget and putting every extra dollar toward debt can work short term, but it often leads to burnout and quitting.

A realistic plan you can stick with will usually take you further.

Closing Credit Cards Too Early

Closing a credit card right after paying it off can feel like the responsible thing to do, but it can sometimes hurt your credit score.

Closing accounts can lower your available credit and shorten your credit history, which may cause a temporary dip.

In many cases, it makes more sense to keep the card open with a zero balance and avoid using it, especially while you are still paying down other cards.

That said, closing a card can be the right choice in some situations. If a card has an annual fee, offers no real benefit, or makes it harder for you to stick to your plan, closing it may be worth it.

Like most parts of paying off credit card debt, this is not one size fits all. The best choice depends on your situation and what helps you stay consistent.

Why Your Credit Card Balance Might Not Be Going Down

If you have started a credit card debt payoff plan and feel like your balance is barely changing, it does not necessarily mean something is wrong. Credit card progress can be slow at first, especially early in the payoff process.

Progress Is Often Slow at the Beginning

Early on, it is common for balances to move slowly, even when you are paying more than the minimum. This is part of how credit card payoff works, and it often improves as balances go down.

Credit Cards Are Still Being Used

This is one of the most common reasons balances feel stuck.

When a card is still being used, the balance has to compete with new charges and interest at the same time. Even small charges can slow progress and make it hard to see results.

If possible, it helps to pause using credit cards while you focus on paying them down. This does not have to be permanent, but it gives your balance room to move and makes progress much easier to see.

Statement Timing Can Hide Progress

Sometimes the balance you see does not reflect your most recent payment yet. Credit cards update on a statement cycle.

If you want to check whether a payment has been applied, look at your transaction history or recent activity in your credit card app rather than just the statement balance. Checking too often can make it feel like nothing is happening, even when it is.

Frequently Asked Questions

What is the fastest way to pay off credit card debt?

The fastest way to pay off credit card debt is to pay more than the minimum on one card while continuing to make minimum payments on the rest.

Using one clear payoff approach, like the snowball or avalanche method, helps your payments work together. What matters most is sticking with the plan. Even small extra payments, when you make them consistently, can add up over time.

Should I save money or pay off credit card debt first?

This depends on your situation. If you do not have any savings at all, having a small emergency fund can help prevent new credit card debt while you are paying balances down.

From there, many people focus on paying down high-interest credit card debt while continuing to build savings gradually.

Should I stop using my credit cards while paying them off?

If possible, pausing credit card use while paying them down can make progress easier to see. When a card is still being used, the balance has to compete with new charges and interest.

This does not have to be permanent, but giving your balances room to move can help your payoff plan work more smoothly.

Next Steps

Paying off credit card debt takes time, but it is doable. Focus on one step at a time, stick with your payoff plan, and let progress build gradually.

Focus on what you can control, make adjustments when needed, and keep moving forward. Momentum often builds after the first card is paid off.

If you want a simple debt payoff calculator that does the math for you, my debt payoff spreadsheet automatically creates a personalized payoff plan based on your budget. It also lets you compare the snowball and avalanche methods and helps you track your payments in one place.