If you’ve ever looked at your bank account and thought, “Wait… where did my money actually go?”

That’s exactly where a zero-based budget example can help.

Especially if you’re living in a high cost of living city, money moves fast. Rent has gone up. Groceries cost more than they used to. Even everyday things like coffee, transportation, and subscriptions add up quickly.

Even a $70,000 or $80,000 salary can feel tight.

That’s where a clearer money system can help.

Zero-based budgeting gives your money a plan. Instead of spending first and figuring it out later, you decide in advance where each dollar will go.

In this guide, I’ll break down how zero-based budgeting works, walk through a simple zero-based budget example with real numbers, and show you how to build one that fits your life.

What Is Zero-Based Budgeting?

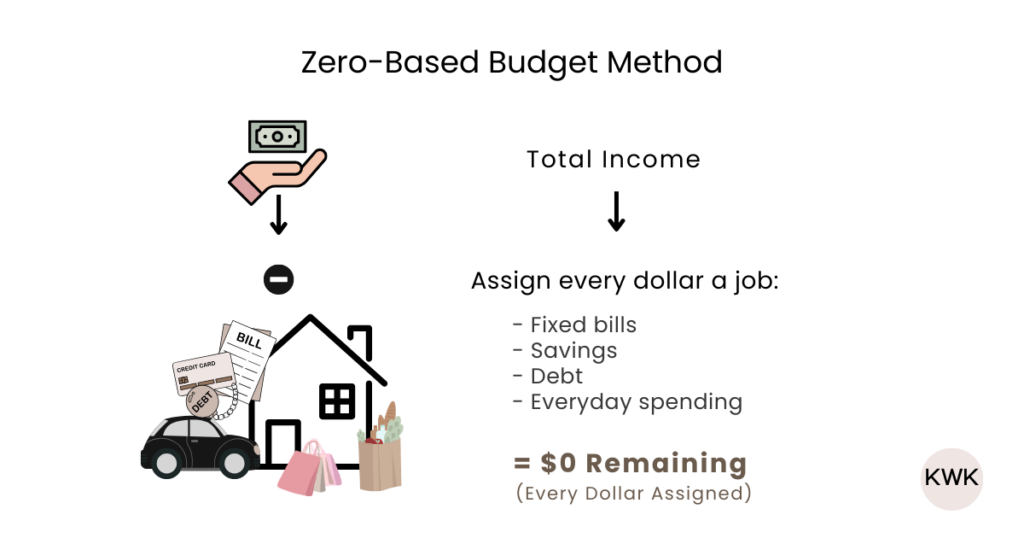

Zero-based budgeting is a budgeting method where you plan your money before the month or pay period begins.

You start with your total take-home pay for the month or paycheck you’re planning. Then you give every dollar a job by assigning it to a specific budget category, like rent, groceries, savings, or debt payments. When you’re done, there is no money left unplanned.

Your income minus your planned expenses equals zero. The “zero” does not mean your bank account is empty. It simply means every dollar has been assigned somewhere.

The idea is not that you are spending all your money. You are deciding ahead of time where it will go. Instead of hoping there is money left at the end of the month or wondering where it went, you decide ahead of time.

You plan first, then spend.

That’s what makes this method different. You assign every dollar before it gets spent, and then track how closely you stick to that plan.

Now let’s look at a zero-based budget example so you can see how this works with actual numbers.

Zero-Based Budget Example (Single, High Cost of Living City, $75,000 Salary)

Let’s walk through a realistic zero-based budget example.

In this scenario, we’ll look at someone who is 29 years old, single, and living in a high cost of living city earning $75,000 per year.

After taxes, health insurance, and deductions, their monthly take-home pay might be around: $4,200 per month.

So for this example, we’re working with $4,200 per month in take-home pay.

Now we assign every dollar a job.

Step 1: Fixed Expenses

These are bills that stay mostly the same each month.

- Rent (shared apartment): $1,850

- Utilities: $120

- Internet: $60

- Cellphone: $80

- Transportation (public transit + occasional rideshare): $150

- Subscriptions: $40

Fixed Total: $2,300

At this point: $4,200 – $2,300 = $1,900 remaining

Step 2: Savings, Goals, and Extra Debt

Most people focus on bills and spending first.

In this example, we’re planning for savings before moving on to variable spending. That means setting aside money for your emergency fund, sinking funds, investments, or any other goals you’re working toward.

You’re paying yourself first.

- Emergency fund: $350

- Travel fund: $100

- Credit card payment (above minimum): $60

- Roth IRA: $300

Savings, Debt, and Investment Total: $810

Now: $1,900 – $810 = $1,090 remaining

Step 3: Variable Expenses

These are everyday spending categories that vary from month to month but still need a realistic estimate.

- Groceries: $450

- Dining out and take out: $250

- Personal and household items: $140

- Gym membership: $50

- Fun Money: $150

- Miscellaneous: $50

- Variable Total: $1,090

Now: $1,090 – $1,090 = $0

Monthly Budget Summary (Zero-Based Budget Example)

- Total Income: $4,200

- Fixed Expenses: $2,300

- Savings & Investments: $810

- Variable Spending: $1,090

Remaining: $0

Here’s what this zero-based budget example highlights:

- Savings and financial goals were treated like a required category

- Fun and everyday spending were included

- Debt was accounted for

- Every dollar was assigned based on needs, priorities, and goals

This is what makes it a zero-based budget.

In real life, your numbers will look different. The structure stays the same.

If you go over budget in a category, you adjust the next month. It doesn’t have to be perfect. You’re building awareness around your spending so you can make better decisions going forward.

If you’d rather see this step by step, I walk through it in this video.

How to Create Your Own Zero-Based Budget

If you want to build your own zero-based budget, first decide what time period you’re budgeting for. That could be the full month or just your next paycheck.

You can use a spreadsheet, a budgeting app, a digital planner, or even pen and paper, whatever makes it easiest for you to stick with.

Then follow these steps to build your plan. After that, you’ll track your actual spending and make adjustments as needed.

Step 1: Write Down Your Take-Home Income

Start with the amount that actually hits your bank account for that time period. You can confirm this by reviewing your recent pay stubs or checking your direct deposits.

If your income varies, use your lowest consistent month or paycheck as your baseline. If you earn more, you can adjust your budget as needed.

Step 2: List Your Fixed Expenses

Now you start planning your budget. Write down bills that stay mostly the same each month:

- Rent or mortgage

- Utilities

- Insurance

- Phone bill

- Minimum debt payments (like student loans, credit cards, car loans, or personal loans)

- Subscriptions

Review your recent bank and credit card transactions to make sure nothing gets missed.

Step 3: Plan for Savings, Goals, and Extra Debt

Savings is not what is left over. It is a planned category.

List the financial goals and debt payments you want to include in this budget:

- Emergency fund

- Retirement contributions

- Travel or sinking funds

- Extra debt payments

Choose numbers that reflect your current priorities. You can adjust after.

Step 4: Estimate Your Variable Expenses

These are everyday spending categories that vary from month to month.

List the variable categories that apply to you, such as:

- Groceries

- Dining out

- Transportation

- Shopping

- Beauty and personal care

- Fun Money

Look at your last two or three months of transactions to get a realistic estimate. Many people underestimate here. If that feels overwhelming, start with the most recent month and refine your numbers over time.

Step 5: Adjust Until You Reach Zero

Now that you’ve listed all your budget categories and estimated amounts, it’s time to make sure everything balances to zero.

Add everything up and check whether your planned amounts fit within your income.

When your income minus your planned expenses equals zero, your zero-based budget is complete. If it doesn’t, you’ll need to adjust. We’ll walk through what that looks like next.

If you’d rather not build this from scratch, you can use my free zero-based budget spreadsheet to follow this exact structure.

How to Track and Adjust a Zero-Based Budget

Now that you’ve built your plan, the next step is tracking your actual spending for the month or paycheck period.

The goal is simple: compare what you planned to what you actually spent in each category.

As the budgeting period begins, check in regularly and update your budget with what you’ve spent. Each time you spend money, subtract the expense from the correct budget category.

For example, if you planned $450 for groceries and you’ve spent $275, you know you have $175 left. If you end up spending $520 instead, you went over by $70.

That’s where the awareness comes in. You’re no longer wondering where your money went. You can clearly see how your spending compares to your plan and adjust as needed.

How Often Should You Track?

You can track weekly, every payday, or on a schedule that works for you. Some people like setting a recurring “money date” to review their spending and update their budget.

It doesn’t have to be daily unless you want it to be. When I first started, I did a quick two to five minute check-in before bed to log expenses and build the habit. After a few months, once it became more routine, I started tracking weekly.

Try not to wait until the very end of the month to review everything. Checking in along the way makes it easier to adjust before things get too far off track.

What Adjusting Actually Looks Like

As you compare your plan to your actual spending, you may need to make small changes.

If one category goes over, you have options:

- Move money from another category

- Adjust that category in your next budget

- You can also look for ways to increase your income if reducing expenses isn’t realistic

Using the grocery example, if you spent $520 instead of $450, you could move $70 from a category that came in under budget. Or you might decide groceries need a higher number going forward. In some cases, increasing your income may also be part of the solution.

If a category is under budget, you also have options:

- Reassign the extra to savings or debt

- Keep it as a buffer

- Lower that category in your next budget

This is how you start noticing patterns.

Maybe groceries are consistently higher than you expect. Maybe subscriptions are costing more than you realized.

That does not mean the budget failed. It means your estimate was off, and now you have a clearer picture of what you actually spent. Adjusting does not mean starting over. It means making small corrections.

At the end of the budgeting period, review everything before creating your next plan.

Over time, your numbers become more accurate because they are based on real data instead of guesses.

Common Zero-Based Budgeting Mistakes

Zero-based budgeting is simple in theory. But in real life, there are a few common mistakes that can make it feel harder than it needs to be.

Here are some of the most common ones.

1. Underestimating Variable Spending

This is probably the biggest one.

It’s easy to set groceries at $300 because that sounds good on paper. But if you’ve consistently been spending $450, that gap will show up quickly.

The point is not to make the numbers look nice. It’s to make them realistic.

If you consistently go over in a category, adjust it.

2. Forgetting Irregular Expenses

Car registration. Gifts. Travel. Annual subscriptions.

These do not happen every month, but they are not surprises either.

If you do not account for them, they will feel like emergencies when they show up.

This is where sinking funds help. Break larger expenses into smaller monthly amounts and assign them a category in your budget.

3. Making the Budget Too Strict

If you give yourself no room for eating out, social plans, or small personal spending, the budget may not last.

A zero-based budget should reflect your real life. If it feels unrealistic, it probably is, and it won’t be sustainable.

4. Not Tracking Regularly

Planning is only half of the process. If you create your budget and never review it, you miss the part that makes it useful.

Tracking does not have to be daily, but it does need to be consistent.

5. Thinking It Has to Be Perfect

Your first zero-based budget will not be perfect.

Your second one probably won’t be either.

It gets better over time because your numbers are based on real spending, not guesses.

You’re not aiming for perfect. You’re aiming to understand your money a little better each month.

Is Zero-Based Budgeting Right for You?

Zero-based budgeting works well if you like having a clear plan for your money and don’t mind tracking where each dollar goes.

It may be a good fit for you if:

- You want to know exactly where your money is going

- You feel like money “disappears” and you want more clarity

- You prefer having a detailed plan

- You want to reach your financial goals faster

That said, it’s not for everyone.

This method might feel harder if:

- You prefer a looser budgeting system

- You dislike tracking spending regularly

- You want something more flexible or percentage-based

Zero-based budgeting is more hands-on than some other approaches. You are actively planning, tracking, and adjusting.

If that sounds like what you need, this approach may be a good fit. It’s personally one of my favorite ways to stay intentional and reach my financial goals faster.

But if it sounds exhausting or hard to stick to, a simpler budgeting system might suit you better.

The best budgeting method is one you can stick with consistently while staying aware of your money and managing it in a way that feels doable.

Frequently Asked Questions

Is zero-based budgeting good for beginners?

Yes, zero-based budgeting can work well for beginners because it clearly shows where every dollar goes, so you’re not guessing anymore. It helps you see exactly what’s happening with your money and gives you more awareness and control early on.

There is a small learning curve at first since you need to check in regularly. Your first few budgets may feel like practice rounds, but it gets easier once you start understanding your spending habits.

What if my income changes every month?

Zero-based budgeting can still work with variable income, but you’ll need to be more conservative.

Instead of budgeting around your highest month, build your plan around the lowest income you can consistently rely on. If you earn more than expected, assign the extra to savings, debt, or other categories once it comes in.

This way you’re adjusting your budget based on what you actually earn to still account for every dollar.

Is zero-based budgeting better than other budgeting methods?

It depends on your personality and goals.

Zero-based budgeting is more hands-on and detailed. It tends to work well for people who like planning and reviewing their numbers regularly.

Others may prefer something more flexible that does not require tracking every dollar.

If you want more clarity and control over your money, zero-based budgeting may be a solid choice.

A Clearer Way to Manage Your Money

If you’ve ever wondered where your money went at the end of the month, zero-based budgeting gives you a way to answer that question.

The zero-based budget example we walked through shows how that looks with real numbers.

It replaces guessing with a plan.

When I first started using zero-based budgeting, it was eye-opening. It was the first time I stopped guessing and saw exactly where my money was going. Instead of saying, “I know I probably spend a lot on shopping or dining out,” I could clearly see the actual dollar amounts in each category.

There’s a big difference between thinking you spend a lot in an area and seeing the exact number in front of you.

Once I saw that, I started making changes based on what actually mattered to me, including my current and future goals. That didn’t mean I cut out shopping or going out completely, because that wouldn’t have been realistic or sustainable. I adjusted the amounts to something I could stick to and shifted money toward what mattered most.

That’s what made the difference.

I wasn’t randomly moving money to savings or cutting expenses and hoping for the best. I had real numbers. I had a plan. I was making decisions on purpose.

And I can confidently say it helped me reach my financial goals faster.

It won’t be perfect the first month. That’s normal. It took me a few months before things started to feel easier. You adjust and improve as you go.

Over time, your budget starts reflecting your real habits and priorities.

If you’d like a simple way to get started, you can use my free monthly zero-based budget template to set up your first plan.